Effective November 1, 2025, Oklahoma will allow credit card surcharges under strict rules: only on credit cards, capped at 2%, and with clear disclosures. But even with these limits, merchants won’t recover full costs—especially on high-fee cards like Amex—and debit surcharges remain illegal. VeriFee recommends cost reduction over surcharging through its Blended Inclusive Pricing, helping businesses lower fees without burdening customers.

Pricing, Regulatory

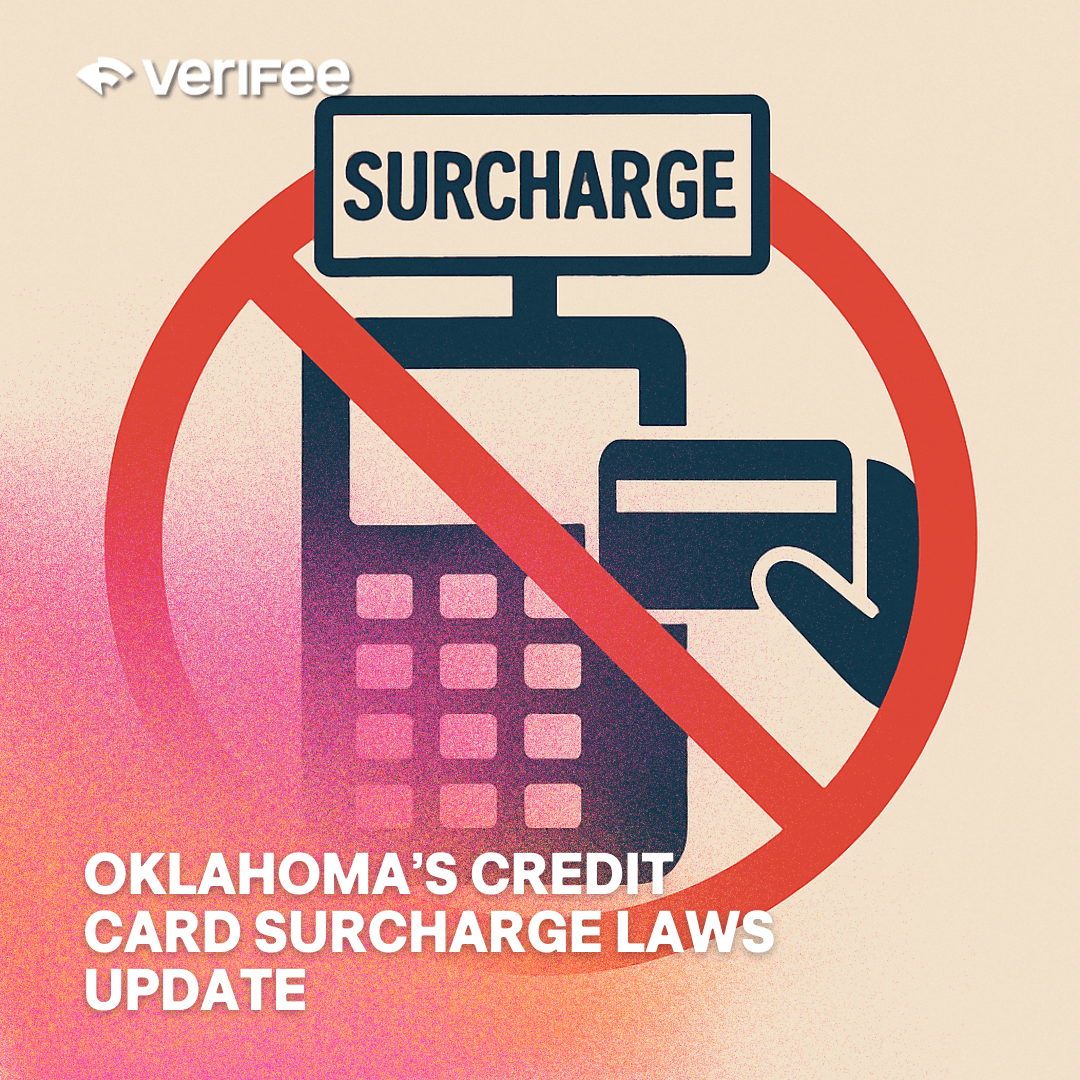

Oklahoma’s Credit Card Surcharge Laws

Jeremy Lessaris

CEO

Clarity, Confusion, and a Better Way Forward

Disclaimer: This information is provided for reference only and does not constitute legal advice. Always consult an attorney with any state-specific legal questions.

Understanding the Landscape

Credit card surcharge laws in Oklahoma have been confusing for both merchants and consumers. Historically, the state prohibited surcharging altogether. But after a series of federal rulings questioned the constitutionality of such bans, enforcement became unclear.

That confusion ends, sort of, on November 1, 2025, when Oklahoma Senate Bill 677 takes effect. The new law will officially allow surcharging, but only under strict conditions and limitations that make it anything but simple.

Is It Legal to Surcharge Credit Card Transactions in Oklahoma?

Yes, beginning November 1, 2025.

Under Senate Bill 677, Oklahoma merchants may impose surcharges on credit card transactions, but only if they follow a very specific set of rules.

Here’s what the new law requires:

- Credit cards only: Surcharges may apply only to credit card transactions, not debit or prepaid cards.

- Choice of payment required: A surcharge is permitted only if the business accepts other forms of payment such as cash, ACH, or check. Customers must have a true choice.

- 2% cap: The surcharge must not exceed the lesser of 2% of the total transaction amount or the actual cost of accepting the card.

Disclosure requirements:

- In-person: Surcharges must be “clearly and conspicuously” displayed at both the point of entry and point of sale.

- Online: Disclosure must appear on both the home page and checkout page.

- Phone: Merchants must provide verbal notice before completing the sale.

Failure to comply with these requirements could expose businesses to fines or enforcement actions. Since “clearly and conspicuously” isn’t precisely defined in the statute, interpretation will likely depend on court rulings, leaving merchants vulnerable to subjective enforcement.

A Narrow Legal Path and a Broad Compliance Burden

While surcharging will be legal, implementing it correctly will be complex. Businesses operating in multiple states now face an increasingly fragmented regulatory map, each state has its own cap, disclosure rule, and definition of “clear notice.”

Section 14A-2-211 still allows cash discounts, meaning merchants can lower prices for cash payments. But to complicate matters further, Visa, Mastercard, and American Express prohibit differential pricing across payment types under their network rules. This means that even if a practice is state-legal, it can still violate card brand compliance, creating another layer of risk. Cash also comes with it’s own costs, read more about Cash vs. Credit Card

Can You Surcharge Debit Card Purchases in Oklahoma?

No. Absolutely not.

Debit card surcharges remain illegal in all 50 states, including Oklahoma. Card brands like Visa, Mastercard, Discover, and American Express explicitly prohibit merchants from surcharging debit or prepaid cards, regardless of state law.

Surcharging Won’t Cover the Cost

Even with Oklahoma’s new rules, surcharging won’t fully offset the cost of credit card acceptance.

High-cost cards, particularly American Express and premium rewards cards, often carry fees well above 2%. Because the state cap is the lesser of 2% or the actual processing cost, merchants won’t recover their true expenses on many transactions.

And remember:

- Debit and prepaid cards can’t be surcharged at all.

- Processors must maintain uniform pricing, meaning you could actually pay more on low-cost transactions to average things out.

- Multi-state businesses must track dozens of unique regulatory frameworks.

In short, even if you surcharge, you’re still paying fees, and likely confusing or frustrating your customers in the process.

A Smarter Approach to Managing Costs

With evolving regulations, complex card brand rules, and growing consumer frustration, surcharging simply creates more problems than it solves.

VeriFee’s approach is smarter, simpler, and more sustainable.

Instead of shifting the burden to your customers, VeriFee reduces your processing costs at the source. Our platform identifies hidden markups, inflated interchange pass-throughs, and unnecessary fees, helping you keep more of what you earn without surcharging, without risk, and without losing customers.

Once your true costs are optimized, VeriFee helps you cost-average your total expenses across all payment methods and treasury services, comparing them against your total revenue. From there, you can adjust your base pricing slightly, usually far less than 2%, to fully offset your costs without complexity or compliance risk.

We call this approach Blended Inclusive Pricing: A transparent, customer-friendly, and fully compliant way to manage payment costs that benefits both you and your customers.

Our 2 cents

Oklahoma’s new surcharge laws may bring clarity to legality, but not to practicality. Passing costs to your customers is never a sustainable strategy, and the only real winners in surcharging are the processors themselves.

If you think you’re paying too much in processing costs, VeriFee can help. Get a free audit today and learn how much you can save, without switching processors, changing your operations, or risking compliance headaches.

Payment processing expenses, explained

See all resources

Payments Glossary